Most clergy pride themselves on being biblically literate. We realize that biblical literacy is not a one-shot affair; we continue to dedicate time and energy to scriptural study throughout our careers.

By Rev. James Cook, CFP®, RICP®, MMBB Financial Planning Specialist

What’s in This Article:

For some families, caregiving follows a familiar rhythm: raising children, enjoying an empty nest, and then caring for aging parents. But today, that timeline has shifted. As people start families later and parents live longer, caregiving has become a dual responsibility for one in four Americans—placing the sandwich generation squarely in the middle.1

The sandwich generation refers to individuals caring for both underage children and aging parents at the same time—often during mid-career years. ² This season of life is deeply meaningful, rooted in love, responsibility, and faith. Yet it can also bring significant financial and emotional strain. So how can families navigate this financial tension with wisdom, stewardship, and hope? In part one of this two-part series, we share the first of seven strategies.

What makes this stage so challenging isn’t simply the cost—it’s the convergence of financial demands. Rising childcare, education, healthcare, housing, and long-term care expenses often overlap at the same time.4

As a result, many caregivers find themselves making difficult trade-offs—cutting back on work hours, delaying retirement contributions, or relying more heavily on savings and credit.3

This “squeeze” can feel overwhelming. But with thoughtful planning and access to the right resources, families can begin to regain a sense of control. In part one of this two-part series, we cover the first three of seven strategies for managing dual caregiver expenses.

1. Start with a Clear Financial Plan

The first step is gaining clarity. Understanding your full financial picture—including income, savings, debt, and long-term goals—provides the foundation for every decision you make.

If possible, have an open conversation with your parent indicating that you will be assisting to determine what resources they have available to provide for their own care. If you will be helping them with financial and medical care decisions, they should consider naming you as a power of attorney who is authorized to act on their behalf if they become incapacitated.

From there, creating a dedicated caregiving budget that separates child-related and eldercare expenses from your other expenses can help you monitor costs and prepare for future needs.

Equally important is setting realistic expectations. Many caregivers feel pressure to meet every need—often at the expense of their own financial security. ³ Thoughtful stewardship means balancing generosity with sustainability.

2. Reduce Childcare Costs with Creative and Public Options

Childcare is often one of the largest expenses families face—but there are ways to manage it more effectively.

Nanny Shares

A growing number of families who use babysitters are turning to nanny shares, where two or more households share the cost of a caregiver. This arrangement allows families to:

Nanny shares offer a practical way to balance quality care with affordability.

Free or Low-Cost Pre-K Programs

Some states and municipalities offer public pre-K programs, often at low or no cost depending on eligibility. These programs provide:

For families with young children, these programs can reduce annual childcare costs.

3. Maximize Tax Credits, Government Benefits, and Workplace Support

Many families navigating dual caregiving responsibilities may not fully leverage the financial support available to them because they are unaware of the full extent of these resources.

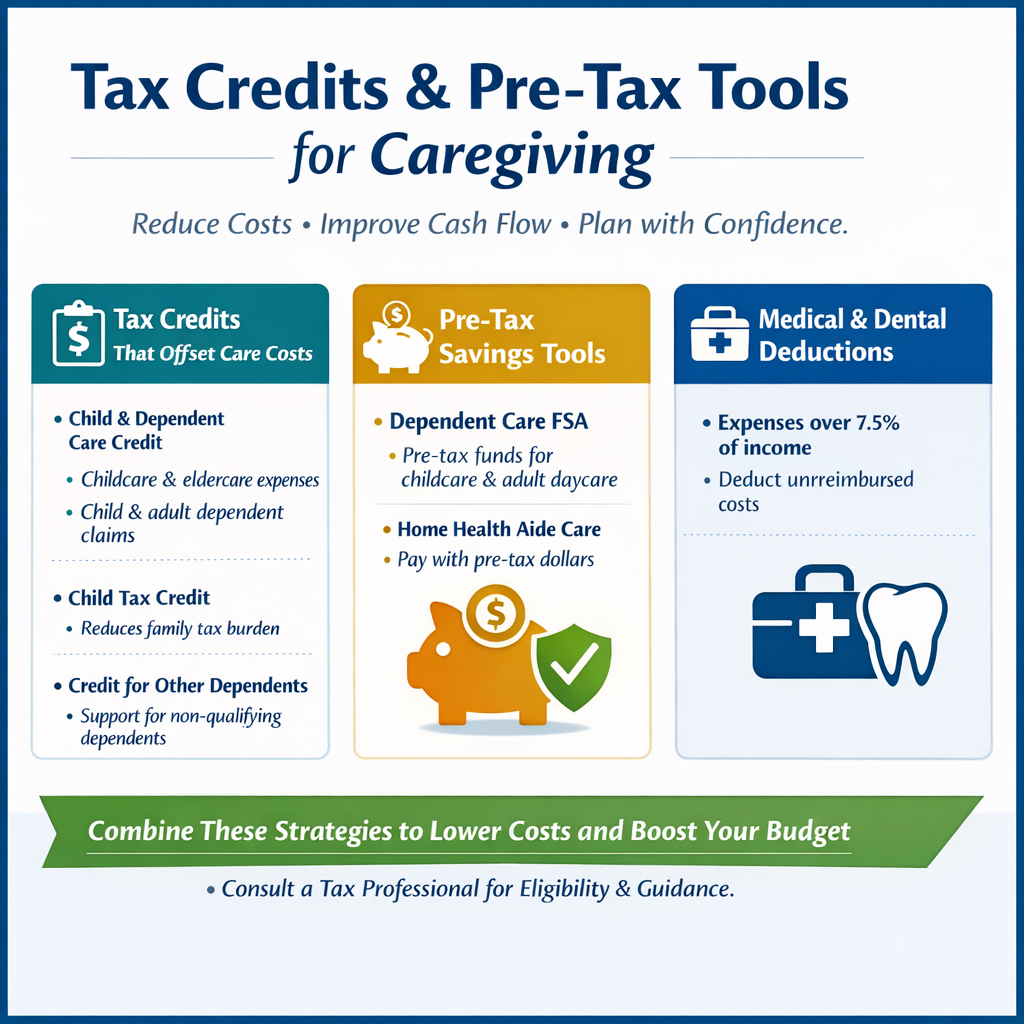

Tax Credits and Pre-Tax Tools

Several tax strategies are designed to ease caregiving costs:

Used together, these tools can improve cash flow and reduce the overall cost of care.

Government Programs

Public programs—particularly for eldercare—can play a critical role in long-term planning. ³

Families may explore:

Because eligibility for Medicaid often depends on income and assets, planning ahead can help ensure access when support is needed.

Workplace Resources

Employers are increasingly adapting to meet the needs of caregiving employees. Common benefits include:

Taking advantage of these resources can help caregivers maintain employment while meeting family obligations.

Watch for part two of this article next month, where we will explore long-term care insurance, trusts and more.

Footnotes

The information in this article is for informational purposes only. Any third-party links included in this article do not constitute an MMBB endorsement. The information contained herein does not constitute any financial, insurance, investment, legal, or tax advice. MMBB is not liable for any success or failure that is directly or indirectly related to the use of the information contained herein.

Translations of any materials into languages other than English are intended solely as a convenience to the non-English-reading public. We have attempted to provide an accurate translation of the original material in English, but due to the nuances in translating to a foreign language, slight differences may exist.

Las traducciones de cualquier material a idiomas que no sean el inglés son para la conveniencia de aquellos que no leen inglés. Hemos intentado proporcionar una traducción precisa del material original en inglés, pero debido a las diferencias de la traducción a un idioma extranjero, pueden existir ligeras diferencias.

You will be linking to another website not owned or operated by MMBB. MMBB is not responsible for the availability or content of this website and does not represent either the linked website or you, should you enter into a transaction. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by MMBB of any information in any hyperlinked site. We encourage you to review their privacy and security policies which may differ from MMBB.

If you “Proceed”, the link will open in a new window.

Next

Next