Most clergy pride themselves on being biblically literate. We realize that biblical literacy is not a one-shot affair; we continue to dedicate time and energy to scriptural study throughout our careers.

When it comes to retirement planning, employees have several investment options that offer tax advantages. Among the most common are Roth accounts and traditional 401(k) and 403(b) accounts. While both are designed to help individuals save for retirement, they differ significantly in how they are taxed and when taxes are paid.

What Are Roth Accounts and How Are They Different from Traditional 401(k) & 403(b) Accounts?

A Roth account, such as a Roth 401(k) or 403(b) account, is a retirement savings vehicle that allows individuals to contribute after-tax dollars. The key benefit of this arrangement is that qualified withdrawals, including earnings, are tax-free in retirement. In contrast, a traditional 401(k) or 403(b) account allows pre-tax contributions, which lowers the employee’s taxable income in the contribution year. However, withdrawals in retirement are taxed as ordinary income.

The major differences between Roth accounts and traditional 401(k) or 403(b) accounts include:

History of Roth Accounts

Roth accounts were introduced in the United States through the Taxpayer Relief Act of 1997. Named after Senator William Roth of Delaware, the Roth IRA was established to encourage long-term retirement savings with the benefit of tax-free withdrawals. Before the introduction of Roth accounts, most retirement savings plans, such as traditional IRAs and 401(k)s, operated on a tax-deferred basis.

In 2006, the Pension Protection Act expanded the Roth concept to employer-sponsored retirement plans, leading to the creation of the Roth 401(k). This allowed employees to contribute to a Roth 401(k) or 403(b) within their workplace retirement plan, combining the higher contribution limits of a 401(k) or 403(b) with the tax-free withdrawal benefits of a Roth IRA.

When Would an Employee Be Better Off Choosing a Roth Account?

Deciding between a Roth account and a traditional 401(k) or 403(b) depends largely on an individual's current and expected future tax situation. Employees may benefit from a Roth account in the following scenarios:

Summing it all up…

Both Roth accounts and traditional 401(k) or 403(b) accounts serve essential roles in retirement planning, but their key difference lies in tax treatment. Roth accounts offer tax-free withdrawals and potential estate planning benefits, making them ideal for individuals who expect their tax rates to rise over time. Traditional 401(k) or 403(b) accounts, on the other hand, provide immediate tax deductions, making them beneficial for high-income earners who anticipate lower tax rates in retirement. Employees should carefully assess their financial goals, income trajectory, and tax situation when choosing between these retirement savings options.

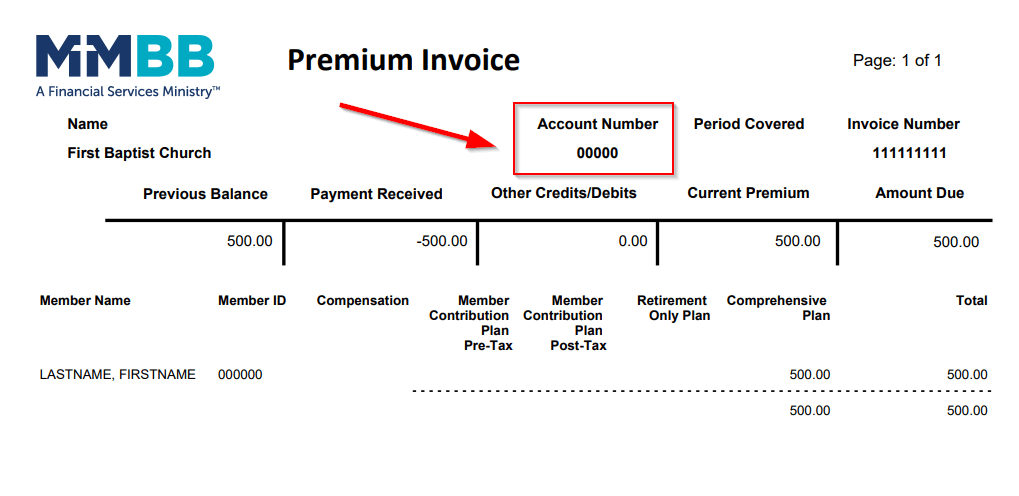

Remember, MMBB accepts Roth 403(b) premiums for employers who support Roth payroll deductions. Some employers may not have the infrastructure for such Roth deductions, so check with your employer if this is an avenue you are considering. It’s important to consult an MMBB financial planning specialist to make an informed decision about whether MMBB’s Roth 403(b) option aligns with your unique circumstances. Remember, financial planning is provided at no cost to members as part of MMBB membership.

The information contained herein is for informational purposes only. While MMBB made every attempt to ensure that the information is accurate, MMBB is not responsible for any errors or omissions or the results obtained from the use of this information. MMBB is not liable for any success or failure that is directly or indirectly related to the use of the information contained herein. The information contained herein does not constitute any financial, insurance, investment, legal, or tax advice. In no event shall, MMBB and/or its fiduciaries, directors, officers, employees, or agents thereof be liable for any special, direct, indirect, consequential, or incidental damages or any damages whatsoever, whether in action of contract, negligence or tort, arising out of or in connection with the use of the information contained herein.

Translations of any materials into languages other than English are intended solely as a convenience to the non-English-reading public. We have attempted to provide an accurate translation of the original material in English, but due to the nuances in translating to a foreign language, slight differences may exist.

Las traducciones de cualquier material a idiomas que no sean el inglés son para la conveniencia de aquellos que no leen inglés. Hemos intentado proporcionar una traducción precisa del material original en inglés, pero debido a las diferencias de la traducción a un idioma extranjero, pueden existir ligeras diferencias.

You will be linking to another website not owned or operated by MMBB. MMBB is not responsible for the availability or content of this website and does not represent either the linked website or you, should you enter into a transaction. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by MMBB of any information in any hyperlinked site. We encourage you to review their privacy and security policies which may differ from MMBB.

If you “Proceed”, the link will open in a new window.

Next

Next